The S&P 500 index declined by 6.44% in the third quarter, bringing its year-to-date return to -5.29%[1]. While this aggregate return is clearly not inspiring, some areas of the market have actually experienced much more precipitous (and perhaps permanent) losses over the last year than this small decline suggests. Most consequentially, the commodities supercycle, a long period of rising commodity prices driven primarily by China’s insatiable desire to (over)build, appears to have come to an end as China’s economy has weakened more rapidly than many predicted. This turn of events has had far reaching consequences and has resulted in carnage in many areas of the market. As of this writing, while the S&P 500 has rebounded to a positive 2.02% year-to-date return, the S&P Metals and Mining Select Industry Index is down by 43.66%, the NYSE Energy index is down by 16.72%, and Brazil, a key emerging market that supplied commodities to China, is down by a whopping 37.10%. Many of the smaller Asian countries that have benefited from China’s rise are also down sharply, ranging from a 13.71% decline in Thailand to a 21.63% decline in Malaysia.

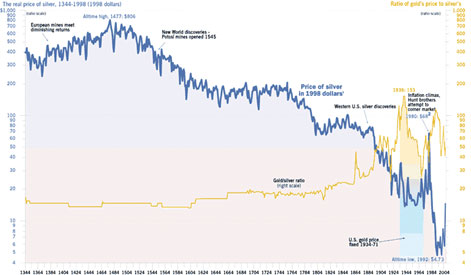

We have largely avoided many of these minefields because of our longstanding aversion to the scary combination of leverage and cyclicality that many commodities businesses possess. However, there is an even more fundamental reason to avoid commodities businesses, even those that are very cheaply priced and conservatively capitalized. To understand why, consider the chart below:[2]

The above graph charts the real (inflation-adjusted) price of silver, but we could have chosen any useful commodity and the picture would look similar. As you can see, the real price has declined dramatically over time. Why is this? It’s because human innovation has caused positive pressure on silver’s supply by lowering the cost of extraction while simultaneously causing negative pressure on demand by creating more substitutes, by increasing recyclability, and by improving production recipes so that they require less silver. The same thing is likely occurring with carbon-based energy sources today as solar and other renewables get cheaper. No useful commodities are immune from this crushing long-term deflationary pressure. Thus, we believe even conservatively capitalized businesses in this industry are likely to generate subpar risk-adjusted returns over time.

So, by avoiding commodities and sticking to our strategy of primarily owning what we believe to be some of the best businesses in the world, with characteristics such as high returns on capital, conservative leverage, steady growth, pricing power, and geographic diversification, we have been able to navigate through this rocky period mostly unscathed, even though many of our businesses have very significant exposure to a number of the most negatively impacted emerging markets. At this point, you might reasonably ask, “But what makes our companies different? Why are the companies we own able to generate such attractive economic characteristics even during these difficult times, and what gives us confidence that they will be able to maintain these advantages over the coming decades?” Below, we’ll lay out our answer to these questions and look at one of our favorite businesses, Colgate, in this context. In doing so, we hope you will gain 1) a better understanding of our analytical framework, including the filters we use to narrow down our investment universe to a select group of world class companies, and 2) more comfort that the companies you own have enduring business models that will thrive for decades to come, even in our fast changing and volatile world.

The Characteristics of the Best Businesses in the World

At their core, we believe the best businesses in the world, those with meaningful pricing power and durably superior economics, have four characteristics:

1) They provide an essential, non-fashion oriented, short repurchase cycle consumable or service. The non-fashion element makes the business more enduring, and the essential nature and short repurchase cycle make its return on capital robust to a variety of economic conditions.

2) The cost of the good the business sells is a small percentage of a person’s or business’s total purchases but with much higher value-add. This element is hugely important because the time and energy cost to the purchaser of negotiating the best deal or searching for substitute brands or products will likely be significantly higher than the cost of almost blindly accepting price increases. When this condition is present, it enables businesses to protect against input cost variability and also to expand their margins over time through consistent price increases.

3) The good’s or service’s pricing is resistant to the deflationary impact of innovation because, in addition to whatever absolute advantage it provides to the customer, it also confers a relative advantage. The best way to illustrate this principle is by comparing goods whose primary value is absolute, such as virtually all of the hardware in our computers, with goods whose primary value is relative, such as goods that enhance social status. Because almost all of the value we derive from the hardware in our computers is performance-related, innovation relentlessly decreases the amount of our disposable income we have to spend on this hardware, even as its performance vastly improves. Goods that enhance social status are different. Social status is a fundamentally relative good, and so the more time and money each person spends to enhance his or her social status, the more everyone else needs to spend to keep up. In a world of innovation, in which the percentage of disposable income required for necessities is going down, we all will have more and more money available to spend on social status. Because of the high value ascribed to this good, many will spend more, leading others to spend more. So, goods that promote social status will likely not only be able to keep up with inflation but actually exceed it over time. However, not all goods that confer social status have durable pricing power. Some are fashion-oriented, such as popular cars like Tesla and many luxury clothing brands. Others confer social status based on their scarcity, and their value erodes as technology makes them more abundant, such as food or electricity. Many are enduring, such as goods that enhance universal cues of youth, health, and beauty like smooth skin, firm muscle tone, clear eyes, lustrous hair, white teeth, and high energy levels.

4) Product penetration is still low worldwide. This characteristic enables the business to reinvest its capital at attractive rates for many years to come.

Colgate

Let’s look at Colgate in terms of these four characteristics. Colgate’s main product is toothpaste, an essential, non-fashion oriented, short repurchase cycle consumable. Additionally, the cost of toothpaste is a small percentage of a person’s total yearly purchases (probably less than twenty dollars a year) but with much higher value-add (prevents potentially thousands of dollars of dental work and all of the time and pain associated with fixing tooth decay). Thirdly, toothpaste is resistant to the deflationary impact of innovation because, in addition to the absolute benefits already discussed, spending more money than others on teeth whitening and other appearance-enhancing oral products confers a universally-recognized relative attractiveness advantage on the spender. It’s no coincidence that Brazil and the U.S. (number one and number two in per capita toothpaste consumption) are also among the highest per capita spenders on plastic surgery. So, to sum up, Colgate sells a product with such favorable characteristics that it appears likely to be able to grow revenue, margins, and profits for a long time to come, even in a mature market like the U.S.

What makes Colgate really exciting, however, is its huge international growth opportunity. There are approximately 1 billion people in the developed world and 6 billion in the developing world and, of those 7 billion people, there are currently over 5 billion people suffering from tooth decay. As wealth spreads to the rest of the developing world, it would be logical to assume that these people will desire to improve the health of their mouths. Furthermore, demographics suggest by 2100 there will be about 11 billion people globally (with most of that population growth estimated to come out of Africa), which means there are an additional 4 billion people yet to be born who are potential customers. Colgate is incredibly well positioned to capitalize on all of this growth. Currently, revenues and profits are 80% international and over 50% emerging markets, and Colgate is the clear toothpaste market leader with a commanding 45% market share worldwide, three times the share of its next biggest competitor. However, even these numbers understate Colgate’s true international dominance. In the U.S., Colgate’s market share is roughly equal to Crest’s at a little over 35%, meaning Colgate’s market share internationally is much higher (over 55% in many markets). Bottom line, in our opinion, Colgate is one of the best businesses in the world, with clear dominance in a market large enough to enable the company to grow to many multiples of its current size.

Though Colgate effortlessly passed through our business quality filters, our work is not quite done. In order to determine whether Colgate is a good investment, we must evaluate one last item: the attractiveness of its forward rate of return. When we run the numbers, we believe the stock is priced to deliver a very high expected return relative both to its business quality and to the returns we expect in the overall stock market. Specifically, Colgate’s currently on offer for a 3.7% shareholder yield with 5-6% revenue growth potential for decades to come. Also, over the last 25 years, operating margins have expanded from 10% to over 20%, and we think they can continue to expand, boosting growth further. Compared to all other investment alternatives currently available, we believe this combination of yield plus growth plus quality will be very hard to beat.

Concluding Remarks

We live in a truly amazing world. Humanity’s ability to innovate has led to exponential improvements in our standard of living by making material goods vastly cheaper and more plentiful, increasing life expectancy, reducing poverty, and reducing disease burdens. While this innovation is good for society as a whole, it leads to a tremendous amount of change that can wreak havoc on individual industries, companies, or people that are not properly positioned to benefit from these changes. As stewards of your and our families’ capital, we will continue to search for and, as long as they are reasonably priced, invest in those companies that possess enduring, timeless attributes that are not just built to last in this fast changing world, but to thrive.

We thank you for your trust and loyalty. Please don’t hesitate to call us if you have any questions or concerns. We appreciate the opportunity to serve you in any way we can.

Sincerely,

The YCG Team

Disclaimer: The specific securities identified and discussed should not be considered a recommendation to purchase or sell any particular security. Rather, this commentary is presented solely for the purpose of illustrating YCG’s investment approach. These commentaries contain our views and opinions at the time such commentaries were written and are subject to change thereafter. The securities discussed do not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. These commentaries may include “forward looking statements” which may or may not be accurate in the long-term. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable. Past performance is no guarantee of future results.

[1] For information on the performance of our separate account composite strategies, please visit www.ycginvestments.com/performance. For information about your specific account performance, please contact us at (512) 505-2347 or email [email protected].

[2] See https://wealthcycles.wordpress.com/2011/10/28/the-real-price-of-silver-1344-1998-1998-dollars/.