During the third quarter, despite a uniquely dysfunctional election season, the S&P 500 generated a solid 3.85% gain.[1] While the randomness of short-term market movements clearly could have yielded a different result, we are nevertheless amused by the apt metaphor that this turn of events offers up. In the face of considerable uncertainty and numerous problems in both the world and the United States, the collective efforts of humanity to better their circumstances moved society’s wealth forward. Taking a longer-term view, this pattern is even clearer, with the average human living a far better life than at any time in the history of the world despite our civilization having encountered wars, famines, plagues, genocides, and natural disasters along the way to today’s exalted position.

But perhaps this trend is at an end. In many ways, today’s problems are some of the gravest we’ve ever faced. Forget about the election. The risks of nuclear terrorism and climate change are commonly seen as both devastating and completely intractable. And if we survive these dual threats, antibiotic resistant super-bacteria and animal-hopping viruses are waiting in the wings to decimate us. Assuming we somehow dodge every one of these potential catastrophes, humankind will still face inevitable decreases in standard of living as our once-in-history discovery of fossil fuels burns away over time. So, is all lost? Should we just accept that our best days are behind us, as 56% of Americans resolutely believe?[2] Before we get too far into our planning process, investment and otherwise, for this new reality, let’s take a trip through time to England around the turn of the 19th century, when a learned man of that age was wrestling with a similar problem.

Malthusian Catastrophe?

Thomas Malthus was an English cleric and scholar who had graduated with honors from Cambridge with a degree in mathematics. A brilliant man, Malthus also excelled in English declamation, Latin, and Greek and was eventually admitted to the most prestigious scientific organization in the world, The Royal Society, members of which have included Isaac Newton, Robert Hooke, and Stephen Hawking. Wanting to put his talents to good use and noticing the improved standard of living of his time, he set about analyzing the sustainability of this improvement in the face of England’s growing population. In 1798, using his impressive mathematical skills and substantial analytical rigor, Thomas Malthus wrote “An Essay on the Principle of Population,” in which he argued that population grows geometrically and food arithmetically. Therefore, he asserted, both the country’s and the world’s populations would soon outstrip their food supplies, leading to mass starvation and abject poverty. Like today’s dire prognostications, Malthus’s argument was quite convincing to many of his contemporaries. Fortunately for us, it ultimately proved spectacularly incorrect.

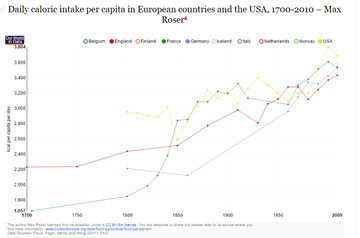

As you can see in the chart below, daily caloric intake per capita in Germany, France, England, and the United States is up by an average of roughly 50% since Malthus’s prediction despite dramatic increases in the populations[3] of these countries.

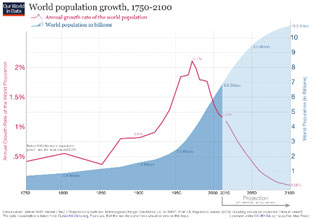

Worldwide, the picture is even more mind-blowing:

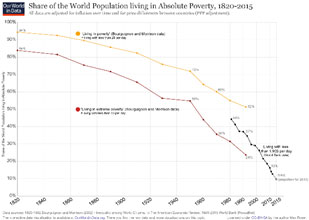

In what is clearly one of the world’s greatest achievements, while the world population has grown from one billion to seven billion since Malthus wrote his essay, absolute poverty levels (defined as living with less than a $1.90 a day) have decreased from roughly 90% of the world population to roughly 10% today.

What Malthus Missed

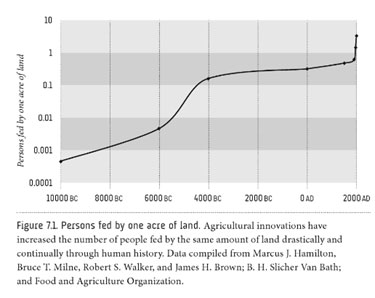

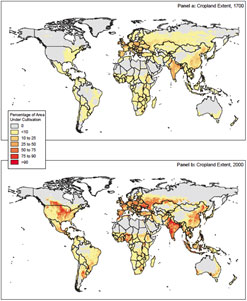

How could Thomas Malthus have gotten this prediction so wrong? He was clearly correct about population growing geometrically, though, contrary to his expectations, the growth rate has slowed over time as many families have freely chosen to have fewer children. However, he completely misjudged humanity’s ability, through innovation, to increase food production, which also has gone up geometrically, but at a much faster rate than population. This rapid increase in food production is a result of 1) huge improvements in yield per acre of cropland and 2) increases in total cropland.

Putting numbers to this point using the charts above, we estimate that, while population has increased seven-fold since 1800, food production has increased by a staggering twenty-fold, made up of a ten-fold improvement in yield per acre and a two-fold improvement in the amount of cropland.[4] In other words, food production has grown at a roughly three times faster rate than population.

Can Innovation Solve Today’s Problems?

While this story is certainly a hopeful one, should this example really assuage our concerns about today’s problems? Aren’t today’s problems much more complex? Won’t they require even more rapid innovation and knowledge accumulation than we achieved in the past? While it is true that the problems of today are more complex than ever, we think modern Malthusians are vastly underestimating both the duration and the magnitude of humanity’s ability to improving its living standards. In our view, they’ve fundamentally misunderstood 1) the total amount of energy and resources available to us if we just have the knowledge to tap into them and 2) the rate at which new knowledge grows relative to the population.

Total Amount of Energy and Resources Available to Us

The first potential constraint on humanity’s ability to improve its living standards is the total amount of energy and resources available. We believe the available amount is far greater than most people realize, as can be seen by looking at the energy potential of the sun, the water resources at our disposal, and the percentage of the earth’s landmass that humans currently inhabit.

Energy is the most important problem that humanity must solve. The discovery of fossil fuels powered our industrial revolution and was a major factor in lifting all but 10% of the world out of poverty. However, fossil fuels are a nonrenewable, scarce resource and, if an alternative power source is not found, will deplete to zero over time. Fortunately, the sun can provide a readily available energy alternative with vastly greater potential than fossil fuels have ever possessed. Just how much greater? Well, to put it in perspective, the earth absorbs more energy from the sun in an hour than all of humanity uses in a year.[5] And the bonus is that it’s clean and will last for at least another 5 billion years.[6]

Once we unlock the power of the sun, all our other resource problems become much more manageable since energy is the key to making other resources available and useful to us. For example, many areas of the world have potable water shortages. However, this problem is not due to a lack of water on planet Earth. Three-quarters of the earth’s surface is covered with water.[7] However, less than 2.75% is fresh water and less than 0.75% is fresh groundwater.[8] We already know how to desalinate and treat water to make it potable, but the process is currently too expensive because of the amount of energy it requires. Therefore, cheap and abundant energy fixes our potable water problem, even without further innovations in the desalination process. Since all elements can be made into all other elements with enough energy, every resource follows this same logic. Cheap and abundant energy, combined with the knowledge of how to transform common elements into uncommon ones, fixes our resource problems.

What about the much more basic problem of humans just running out of room? Well, because most people prefer to live in cities, only 10% of the world’s land surface holds 95% of the world’s population.[9] In the countries where more people live in rural areas, the inhabitants generally exhibit the same preference as the rest of the world and are quickly urbanizing. Thus, humanity has plenty of room in which to expand if needed. Moreover, even cities have the potential to house significantly larger populations since a huge percentage of these cities’ land is devoted to parking spaces and streets (about fifty percent on average and sometimes as much as two-thirds).[10] Given that today’s cars are parked 95% of the time,[11] autonomous driving and ridesharing could drastically reduce the need for automobile-related land.

Rate at which New Knowledge Grows Relative to the Population

The second potential constraint on humanity’s ability to improve its living standards is the rate at which new knowledge grows relative to the population. We believe knowledge growth is extremely likely to outstrip population growth and that knowledge’s advantage could continue virtually indefinitely. To understand why, let’s compare their growth functions. Population growth is a function of the number of people born and the number of people who die. Knowledge growth, by contrast, is a function of innovation (i.e. the creation and mixing of ideas), which, in turn, is a function of the number of humans, their idea generating capabilities, and their connections with one another. While it may not yet be apparent, the key difference between these growth functions is the “connections” variable. A concrete example will hopefully illuminate this difference.

For simplicity’s sake, let’s assume a society in which each person can come up with one idea and each person can mix their idea with another’s to create a new idea. So, in a society of 1 person, the number of ideas is 1 + 0 mixings, which equals 1 total idea. In a society of 2 people, the number of ideas is 2 + 1 mixing, which equals 3 total ideas. In a society of 3 people, the number of ideas is 3 + 3 mixings, which equals 6 ideas, and, in a society of 4 people, the number of ideas is 4 + 6 mixings, which equals 10 total ideas. As you can see, the rate of growth of people is fast, but the rate of growth of ideas is faster. And that is because of rapid growth in mixing possibilities as the population gets larger. Even though the number of ideas per person (1) didn’t change and thus the total number of non-mixed ideas grew in line with the population, the number of mixing possibilities rapidly balloons to much greater than the population.

Scientists have studied this phenomenon and come up with a formula called Metcalfe’s law[12] that allows us to figure out how many mixings are possible as the population gets larger. The numbers become large very quickly. At 100 people, the number of ideas in the society would be 100 (1 per person) plus 4,950 mixing possibilities, which equals 5,050 total ideas. In a world of 7 billion people (the current number on planet Earth today), the number of idea possibilities is mind-blowing at 2.45^19. Basically, the mixing possibilities grow so exponentially that we’ve gone from a scenario of 1 person in the world in which there is 1 idea per person to a society of 100 people in which there are 50.5 ideas per person to a society of 7 billion people in which there are 3.5 billion ideas per person. Not all these ideas are good, of course, but the good ones almost always spread since knowledge really is power. Thus, it should be no surprise that humanity’s standard of living has improved over time since the number of ideas per person, which include everything from ideas about how to cheaply feed, clothe, and shelter ourselves to ideas about how to govern ourselves to ideas about how to achieve joy, has also been rapidly increasing.

What’s perhaps most amazing about this exercise is that it’s extremely conservative in its assessment of society’s idea generation capability because it doesn’t assume any mixing of mixed ideas (i.e. remixing). But, in the real world, we CAN remix ideas. Thus, in the society of 100 people that we mentioned earlier, they created 4,950 ideas by mixing their 100 ideas. In a world with remixing capabilities, they can mix those new 4,950 ideas with each other and with the 100 original ideas. And then, they can take the resulting ideas from those mixtures and remix them, leading to an unlimited combinatorial potential of ideas, which is why the information age has been so powerful. As more and more people get educated[13] and connected[14] and as more and more computers are built to scour the world for ideas and to remix them, the number of ideas in the world is exploding. In the next section of this letter, we’ll look at the investing implications of this idea explosion.

Investing Implications

First, the standard of living of the average person has gotten massively better over the course of history, and innovation is the driving force behind this change. Because of the total resources and energy available to us, the unlimited combinatorial power of ideas, and the increasing population, education, and connectivity of the world, we believe growth in worldwide wealth per capita is very likely to continue to increase for a long time and potentially at a faster and faster rate. Thus, we believe that the rewards from owning reasonably-priced businesses that benefit from long term worldwide wealth per capita growth are likely to be quite substantial.

Second, and paradoxically, the difficulty of figuring out which businesses will benefit from this growth has probably never been higher. The average lifespan of an S&P 500 company has already dropped from 67 years in the 1920s to 15 years today,[15] and today’s rapid acceleration in idea generation may lead to even faster and more profound changes in our economy than we saw over the last one hundred years. Thus, we as investors need to put more and more emphasis on investing in businesses whose economics are least likely to change for the worse in the face of this rapid technological progress, and our study of the history of innovation can help us to identify these businesses.

Innovation and Declining Prices

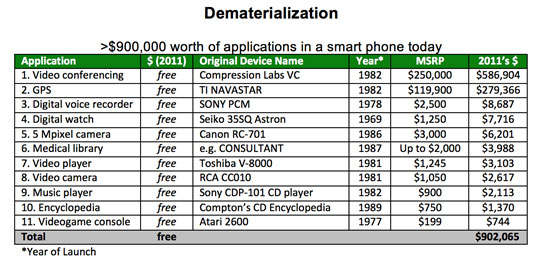

Warren Buffett was once quoted as saying, “The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business. And if you have to have a prayer session before raising the price by 10 percent, then you’ve got a terrible business.”[16] We largely agree with this sentiment. What’s interesting about innovation is that it works directly contrary to these goals. As we saw in our analysis of food production per acre at the beginning of this letter, new ideas enable us to get more and more stuff out of the same amount of resources. The inverse of this statement is that the same amount of stuff costs us less in resources (money, time, labor). Thus, almost everything we buy is getting cheaper to produce over time. Furthermore, if idea generation is speeding up, then everything is probably getting cheaper to produce at an accelerating rate. Peter Diamandis, the founder of the X Prize Foundation and Singularity University, recently wrote an article[17] that describes this process as demonetization. He begins with a fascinating chart (reproduced below) that outlines how many formerly expensive products are now essentially free on your smartphone.

While some of the businesses that sold these products have been able to innovate fast enough to replace the revenues lost as a result of these price declines, many others are far less profitable than they once were and, in some cases, are bankrupt. Unfortunately, it’s very difficult to predict which companies will be the successful innovators in advance.

In the remainder of Diamandis’s article, he predicts that future demonetization could wreak havoc on many large industries such as energy, transportation, media, and healthcare. Based on our study of innovation, we agree.

For instance, while our discussion earlier in the letter about using sunlight to power human civilization may have seemed hopeful but ultimately unrealistic, the data suggests not only that cheap and abundant solar power is possible, but that it’s possible now. In fact, the cheapest solar plants are now cheaper than all other energy plants, and not by a little. They’re so inexpensive that the cheapest solar plant, which includes all the property, equipment and people required to run the plant, is now cheaper than traditional power plants’ fossil fuel cost alone.[18] If costs keep falling, which we have every reason to expect they will, solar could dramatically disrupt the utility industry. Additionally, electric vehicles, which are basically batteries on wheels, are already a reality and their costs are declining so rapidly that they may be cheaper than the cheapest new internal combustion vehicle by 2030.[19] This change alone could be quite damaging to the profit models of the automobile, auto parts, trucking, and auto insurance industries. However, combined with autonomous cars and ridesharing, it could be absolutely devastating. Finally, the digitalization of media is leading to far more videos, articles, and songs being produced than our finite attention could ever consume, and most of this media is free, having been generated by users not for money, but for fun. All these changes are arguably happening now, but, in the future, the disruption could be even more extreme. Significantly improved artificial intelligence, virtual reality, and 3-D printing could transform society to a far greater degree than even the case we’ve laid out here.

So, in a world in which wealth per capita is increasing at the same time that information and stuff are becoming ever cheaper and more abundant, which businesses are likely to pass Warren Buffett’s pricing power test? As has always been the case, people are willing to pay for the scarce and desired resource. Increasingly, this scarce resource is our time. There are only so many hours in a day to allocate and the ways to allocate these hours are endless and growing exponentially.

Thus, we think one category of business models whose economics are likely to stay the same or improve is businesses focused on value-added filtering, which we define as those selling filtering products that are cheap relative to a person’s or business’s disposable income and relative to the value the filter provides. We can already see the shift in economic value added in areas like media. Newspapers, magazines, and movie studios are finding it increasingly difficult to monetize video and word content, but filters such a Facebook and Google are generating huge profits because, at the cost of a couple of ads or a few dollars, they allow us to efficiently and quickly find content relevant to us. In a world with an increasingly diverse and complex set of companies and risks, brokers such as Aon, Goldman Sachs, and Schwab perform this same filtering function for buyers and sellers of insurance and financial products. Additionally, many cheap, disposable, one-hundred-year-old products like Colgate toothpaste, Frito-Lay chips, Nestle chocolates, and Clorox cleaning products should continue to thrive because, for only a few cents, they serve as time-saving safety and efficacy filters. National banks such as Wells Fargo and JP Morgan save customers time with superior technology, vast branch networks, broad product offerings, and reputations for financial soundness. Mastercard and Visa serve as low-cost fraud and convenience filters to seamlessly conduct transactions. Finally, in a world of increasing globalization and an expanding circle of human connections, many people use luxury goods as a filter to identify desirable business and life partners. Unlike other products, however, luxury goods have the unique and favorable property that their value is positively correlated with their price. Thus, in a world of increasing wealth per capita, they will only continue to serve as useful filters if their prices increase as well, meeting Warren Buffett’s pricing power test in spades.

Another category that we believe possesses pricing power is businesses that sell unique and hard-to-replicate but widely desired experiences. One of the clearest examples of this transition from stuff to experiences is the music industry. It is much more difficult for artists and businesses to generate revenue from selling songs, but artists and companies like Live Nation can still make a lot of money on concerts. Additionally, the average movie’s profitability appears to be declining over time, whereas theme parks where beloved characters come alive continue to successfully raise prices over time. This experiential halo effect even ends up benefiting the beloved characters’ movies. The movies that have experienced the least pricing pressure appear to be the ones connected to characters with long cultural histories, with opportunities through toys and collectibles to integrate them into a fan’s life, and with experiences where the characters come alive. Likewise, many branded consumer goods, such as cola, alcohol, chocolate, coffee, shoes, and clothes, connect people to their tribe in a way that makes them loyal to the products. These loyalties can sometimes be quite fierce and have proved remarkably persistent over time because of their connection with social status, which leads us to luxury goods. Besides serving as filters, luxury goods connect their owners to culturally significant places and people while also invoking pride in a very satisfying way. These attributes add to pricing power and enable them to charge far more than other products without these associations. Shoes are cheap and abundant, but, for many people, feeling connected to a favorite basketball player or team is worth a hefty price premium. There are many affordable jewelry options, but Cartier jewelry connects its owners with Paris from 1850 to the present and with Grace Kelly and other royalty. Additionally, many people who receive these brands as gifts are deeply moved since they see them as costly and thus hard-to-fake signals of the esteem in which they are held by the gift-giver.

Before proceeding to our concluding remarks, we’d like to offer a few caveats to this pricing power analysis. First, the list of businesses above is certainly not exhaustive. There are many other business models that will survive and prosper in the future, some of whose competitive advantages we will be able to understand and some of whose we won’t. Second, we occasionally invest in businesses with more future uncertainty provided they are sufficiently inexpensive relative to other investment alternatives. After all, our goal is to generate superior risk-adjusted returns, and the price paid for a business is clearly one of the most important factors in achieving this objective. These few caveats aside, we nevertheless believe that accelerating technological change is making it increasingly difficult to achieve attractive investment returns by investing in businesses with declining or questionable pricing power, and we hope our analysis of innovation and its investing implications provides a clearer picture of the types of business that we believe meet our pricing power test.

Concluding Remarks

Because the salacious, the sadistic, and the scary tap into deep primal needs and fears, they are more attention-demanding than their opposites. Media coverage further exacerbates the mindshare that these events commandeer. Since our worldviews and “risk maps” are strongly correlated with mindshare, it’s no wonder most of us are negative on the future of the world.[20] There is no doubt that the world has problems. Many of these problems are more complex, alarming, and seemingly intractable than ever. However, in focusing so much on our problems, we’re missing the enormous progress that the world has made over time. More importantly, we’re missing that the underlying cause of this progress, the number of new ideas created and put into practice, is far from running out of steam. In fact, innovation is stronger than it’s ever been. Thus, in our view, not only is the world likely to get better in the future, it’s never been more likely to get better. Moreover, we believe it’s more likely than not to get better and better at a faster and faster rate. Finally, while there are risks to today’s businesses from the rapid technological change that this idea explosion drives, there are many opportunities as well. We believe we’ve constructed a portfolio of reasonably priced businesses that are robust to this technological change, and we are working to improve this robustness every day.

As always, please feel free to call us with any questions or concerns, and we thank you for your trust.

Sincerely,

The YCG Team

Disclaimer: The specific securities identified and discussed should not be considered a recommendation to purchase or sell any particular security nor were they selected based on profitability. Rather, this commentary is presented solely for the purpose of illustrating YCG’s investment approach. These commentaries contain our views and opinions at the time such commentaries were written and are subject to change thereafter. The securities discussed do not necessarily reflect current recommendations nor do they represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. These commentaries may include “forward looking statements” which may or may not be accurate in the long-term. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable. S&P stands for Standard & Poors. All S&P data is provided “as is.” In no event, shall S&P, its affiliates or any S&P data provider have any liability of any kind in connection with the S&P data. Past performance is no guarantee of future results.

[1] For information on the performance of our separate account composite strategies, please visit www.ycginvestments.com/performance. For information about your specific account performance, please contact us at (512) 505-2347 or email [email protected].

[2] See http://money.cnn.com/2016/01/28/news/economy/donald-trump-bernie-sanders-us-economy/.

[3] The USA’s population rose from 5 million in 1800 to 324 million today. Over the same time period, England, Malthus’s country of origin, increased its population from 8 million to 55 million, Germany increased its population from 22 million to 81 million, and France increased its population from 30 million to 65 million. See https://en.wikipedia.org/wiki/Demography_of_the_United_States, http://ukpopulation2016.com/england, https://en.wikipedia.org/wiki/Demography_of_England, http://www.populstat.info/Europe/germanyc.htm, http://www.worldometers.info/world-population/germany-population/, and https://en.wikipedia.org/wiki/Demographics_of_France.

[4] Yield per acre and cropland charts are reproduced from The Infinite Resource by Ramez Naam and https://ourworldindata.org/land-use-in-agriculture/, respectively.

[5] See https://en.wikipedia.org/wiki/Solar_energy and https://en.wikipedia.org/wiki/World_energy_consumption.

[6] See http://www.bbc.com/earth/story/20150323-how-long-will-life-on-earth-last.

[7] See http://water.usgs.gov/edu/earthhowmuch.html.

[8] See https://en.wikipedia.org/wiki/Fresh_water.

[9] See https://www.quora.com/Philosophy-of-Everyday-Life-What-percentage-of-the-worlds-land-is-populated-by-humans.

[10] See http://www.planetizen.com/node/72454/land-vehicles-or-people, http://oldurbanist.blogspot.com/2011/12/we-are-25-looking-at-street-area.html, and http://www.vtpi.org/land.pdf.

[11] See http://fortune.com/2016/03/13/cars-parked-95-percent-of-time/.

[12] See https://en.wikipedia.org/wiki/Metcalfe%27s_law.

[13] See https://ourworldindata.org/global-rise-of-education.

[14] See https://ourworldindata.org/internet.

[15] See http://www.bbc.com/news/business-16611040.

[16] See http://www.businessinsider.com/warren-buffett-pricing-power-beats-good-management-berkshire-hathaway-2011-2.

[17] See http://singularityhub.com/2016/07/18/why-the-cost-of-living-is-poised-to-plummet-in-the-next-20-years/.

[18] See http://rameznaam.com/2016/09/21/new-record-low-solar-price-in-abu-dhabi-costs-plunging-faster-than-expected/.

[19] See https://www.youtube.com/watch?v=EECxyL4gCEY. Tony Seba, a Stanford University instructor, is even more optimistic about electric vehicle costs, as can be seen here: https://www.youtube.com/watch?v=Kxryv2XrnqM.

[20] See http://money.cnn.com/2016/01/28/news/economy/donald-trump-bernie-sanders-us-economy/.