The S&P 500 continued its upward march during the third quarter, posting a 4.48% gain.[1]

In our last letter, we concluded by outlining the core tenets of our investment strategy. In preparing to write this one, we noticed a slight but important adjustment to what we wrote, so we’ll repeat the relevant section below:

“We continue to 1) focus mainly on high market share, conservatively levered, stable businesses with enduring pricing power and compelling long-term growth opportunities; 2) attempt to acquire these businesses at reasonable valuations when they are experiencing short-term macro-economic and/or operational problems; and 3) stay fully invested in most market environments.”

In rereading this section, we would modify 2) in our core investment strategy to read “attempt to acquire these businesses at reasonable valuations when they are experiencing or when investors fear they will soon experience short-term macro-economic and/or operational problems.” Both these conditions (the actual experience of problems and the anticipation of problems) generally lead market participants to shorten their investment time frames and to overconfidently attempt to time their entry into and exit out of positions, creating opportunities for long-term investors. In a real-time example of this market dynamic, we believe fears of imminent macroeconomic weakness recently gave us the opportunity to acquire CBRE Group (CBG) at what we believe was an attractive price.

CBRE Group

CBRE Group is the largest commercial real estate brokerage in the world. We believe it is a great business because 1) the commercial real estate market has favorable long-term growth tailwinds; 2) the brokerage business model is excellent; 3) CBRE has unique scale, dominance, and expertise in the industry; and 4) CBRE management is aligned with shareholders and executing a strategy that we believe is likely to increase business value over time.

The first reason that CBRE is a great business, in our opinion, is that it operates in an industry with favorable long-term growth tailwinds. The most important component of this growth is aggregate commercial real estate’s historical inflation protection.[2] In other words, commercial real estate has exhibited pricing power. Interestingly, despite its seemingly more direct connection to economic activity, commercial real estate is not a special case, as aggregate residential real estate prices have also grown at rates roughly equal to inflation.2 We believe real estate derives this ability to raise prices from its positional characteristics. Like beauty, another classic positional good, real estate derives its value much less from some absolute standard of livability than from its positioning relative to other people. In beauty’s case, all else equal, the more attractive you are relative to other people, the more successful you’ll be in competing for mates and economic resources. In real estate’s case, all else equal, the more proximate you are to other people, the more wealth you’ll generate and people you’ll meet, which, in turn, enhances your and your family’s survival and reproduction chances.[3] There are other factors that create value in real estate, such as the value of the economic resources underlying it in the case of oil-rich land or the status-signaling value of owning an island, but the vast majority of the long-term value of real estate derives from its proximity to other people.

What explains this linkage in real estate value and population density, and will it continue into the indefinite future? Ultimately, the fundamental reason for this linkage is the positive-sum nature of cooperation, in which cooperation between individuals leads to greater gains in wealth than can be achieved by those same individuals if they act independently. For example, a group of hunters are far more likely to survive over time if they team up to hunt food and then share it amongst themselves than if they each try to capture their own prey, many examples of which are larger and fiercer than any individual human. Over human history, this positive-sum nature of cooperation has led to an increased frequency, scale, and intimacy of cooperation through a positively reinforcing cycle of increased human sociality, first through the genes as the more social among us were the ones who were more likely to survive and reproduce and then through culture as various societal innovations like government monopoly of the legitimate use of physical force, capitalism, property rights, and democracy served to incentivize prosocial (positive-sum) behavior like cooperation and disincentivize anti-social (negative or zero sum) behavior like murder. Additionally, many of our modern technologies such as farming, electricity, air-conditioning, infrastructure, the internet, and medicine have accelerated our increasing proximity by reducing many of the resource constraints and other negative externalities that limit population density.

Therefore, as in other arms races, because population density is correlated with wealth creation, and status is correlated with wealth, we believe humans, on average, will contribute a constant or rising share of their income to real estate over time since not doing so would mean losing status and economic opportunity relative to those who do. We believe this dynamic should enable long-term real estate spending to grow at least as fast as global GDP, with this increased spending being divided between existing real estate (through higher aggregate prices) and new real estate (driven by population growth and perhaps increased commercial and residential square footage per capita as wealth per capita grows).[4] Importantly, CBRE is over-indexed to urban areas, which should experience faster growth than the commercial real estate market overall because of the continued migration from villages to cities, particularly in developing countries. By 2030, roughly 1 billion more people are expected to live in cities while rural populations are expected to remain flat, increasing the global proportion of city-dwellers to over 60%. By 2050, 70% of the world’s population will be urban.[5]

The second reason that we believe CBRE is a great business is that the brokerage business model possesses many wonderful attributes, including network effects, brand value, and low capital intensity. First, like many other networks, brokerages connect buyers and sellers of various goods and services. This connection is value-added if it lowers the transaction costs of the buyer and/or the seller of these services. In many cases, it lowers these transaction costs dramatically. To understand how this reduction in cost occurs, let’s examine CBRE’s industry, commercial real estate. Most businesses need real estate for their offices, their stores, and their factories, but, for many of these businesses, transacting in real estate is neither their core competency nor a frequent activity. Thus, it would be a bad investment for them to maintain the necessary knowledge, staff, and relationships with other real estate participants. Instead, it is much cheaper and more efficient for an intermediary such as CBRE to form relationships with the various business and real estate owners. By aggregating these relationships, it can amortize its costs against far more transactions than any of the individual businesses can on their own, reducing the real estate costs of all participants while increasing its own economic profits. Additionally, because CBRE’s value to buyers increases with the number of sellers in its network and its value to sellers increases with the number of buyers in its network, CBRE’s competitive advantages strengthen as it scales. Furthermore, as it becomes one of the first commercial real estate brokerages to globalize, we believe CBRE is experiencing a step-change in its competitive advantages since the regulatory, cultural, and legal complexity of cross-border activity requires a much larger investment that prices out many smaller players.

The second favorable attribute of the brokerage business model is brand value. Brands such as CBRE command pricing power if they lower customers’ search costs and/or enhance their status. Google, Amazon, Facebook, and a host of other companies are eroding the first of these advantages by lowering search costs for consumers. When combined with the big technology firms’ success in lowering start-up/distribution costs for new competitors, this reduction in search costs has caused increased market fragmentation in many branded industries as niche brands with varied value propositions can often better serve disparate consumers than one-size-fits-all solutions. Nevertheless, we believe high relative mindshare will continue to confer an advantage on many well-known brands, especially when the due diligence of a good, service, or experience is time-intensive and complex, as is the case in commercial real estate brokerage. In contrast to search costs, we believe status-enhancement, the second source of brand pricing power, may be increasing in importance over time. Increasing urbanization and globalization create more interactions with strangers, making universal signals of status more valuable. Additionally, social media appears to be adept at both tuning up status-signaling desires and providing more opportunities to fulfill these impulses. Status-signaling generally breaks down into two categories: 1) advertising one’s loyalty to a tribe, and 2) advertising one’s positioning within a tribe. One effective way to advertise one’s positioning within a tribe is to associate with other high-status members. In a business setting, market leaders and other types of high-achieving firms are high-status. Thus, for example, getting Goldman Sachs to perform your IPO or working with CBRE on your real estate sale can raise your status as a businessperson, making it worthwhile to pay slightly more to attach your company to the desirable brand. Furthermore, in some business situations, such as in principal-agent relationships, the purchaser uses the brand more as a tool to maintain status than to gain it. In these cases, agents (employees) are acting on behalf of a principal (the owner) to select service providers. Agents generally prefer the easiest and safest decisions on service provider choices such as commercial real estate brokerage because the upside to the agent’s career from a good unconventional choice rarely compensates for the downside to his/her career from a poor one. Thus, from the agent’s perspective, the unconventional choice is not worth the extra effort and risk, even in cases where the conventional choice is more expensive. This common principal-agent problem birthed the popular aphorism, “You never get fired for choosing IBM.” Increasingly, large pensions and endowments, which are even more susceptible to the brand effects discussed above, are investing in commercial real estate.[6] We believe this trend will support and perhaps increase the value of CBRE’s brand.

One interesting implication of brokerage network effects and brand value is that, contrary to many other businesses, we believe brokerages generally add value by consolidating. Since commercial real estate brokerage has a large relationship component to it, the main reason for CBRE to buy a smaller brokerage is to gain access to the brokers and their existing customer relationships. This benefits CBRE greatly because of the geometric effects of increasing its network of relationships. Additionally, the acquisition likely increases the productivity of the individual brokers since they can leverage CBRE’s superior brand and resources to more easily acquire new customers. We believe these positive effects outweigh the traditional negatives of acquisitions such as CEOs’ incentives to empire-build and the difficulties of integrating separate organizational cultures.

Finally, brokerages are capital-lite since a substantial piece of their value is in the brokers they hire. This characteristic enables brokerages to return high percentages of earnings to shareholders even as they grow. Also, because people are a significant portion of the cost structure, they can generally continue to produce cash even in bad downturns since they can pay their people less or downsize. Finally, they don’t take meaningful capital risk on the properties they broker and service, which generally require significant leverage to generate attractive returns and thus force investors to risk bankruptcy in bad downturns. Brokerages, on the other hand, because of the favorable characteristics already mentioned, don’t require leverage to generate attractive returns but can safely support moderate amounts of it.

While we believe the brokerage business model has many positive characteristics, no business is completely future-proof. We think there are three main risks to the long-term economics of the brokerage business model, all of which we believe are low probability in CBRE’s case given the dynamics of the commercial real estate market.

First, the brokerage’s end market could shrink. As an example, this risk may soon befall the auto insurance industry. The widespread adoption of autonomous vehicles would dramatically reduce the need for personal auto insurance, severely impairing the value of brokerages focused on selling this product. In contrast, because of the already-discussed causal relationship between population density and wealth creation, we believe the commercial real estate market will continue to grow over time.

Another risk to brokerages is customers or suppliers becoming much more concentrated, as currently appears to be occurring in the advertising industry. The advertising agencies began as intermediaries between businesses looking to purchase advertising and the newspaper industry, which supplied the attention of millions of consumers. Instead of each company forming relationships with the thousands of newspapers in the country, it made sense for the companies and newspapers to go through a middleman. Now, with Google and Facebook taking more and more share of the advertising market and possessing a virtual duopoly in the digital space, advertising agencies’ value proposition is declining. We believe the commercial real estate market is at low risk of owner, buyer, or lessor concentration given both the size of the industry and the variety of interested parties.

The final potential risk to the brokerage model would be a disintermediation of the brokering function. We believe this risk declines the more consequential, expensive to reverse, complex/bespoke, and infrequent the transaction. Commercial real estate purchases are consequential (large dollar transactions), difficult and expensive to reverse (illiquidity + substantial brokerage fees), and complex/bespoke given the wide variety of zoning, demographic, regulatory, tax, topographical, and local supply/demand considerations. They are also quite infrequent, with many buildings and/or leases turning over on the timescale of years or decades. All these factors make it hard to generate an efficiently-priced and liquid market in each property, increasing the purchaser’s need for outside expertise. We believe these factors lead to few scalable solutions that could disrupt the business. Contrast this situation with the travel agency, where Priceline and other competitors are clearly disintermediating the traditional brokerage model. In the travel industry, each individual hotel, airline, and rental car purchase is generally of low consequence in terms of money, importance to overall life, and even experience of the trip since the city, business meeting, or social event is often the main attraction, not the hotel. Additionally, travel purchases are relatively cheap and easy to reverse because they are short-term rentals that automatically expire after the reservation period ends and because high turnover of rooms, seats, and cars enables providers to offer 24-hour cancellation policies, seamless online or telephone cancellation, and fees for cancellation that, while annoying relative to the total cost of the flight or hotel, are still relatively small compared to a person’s or business’s annual income. Furthermore, the contract terms on these purchases are generally standard and simple. Finally, the high turnover of rooms, seats, and cars generates efficient markets with transparent pricing as well as high numbers of online reviews that enable customers to easily research the differences between the various options available to them. In summary, using the above framework, we think commercial real estate brokerage has low risk of technological disintermediation.

The third reason we believe CBRE is a great business is that it has unique scale, dominance, and expertise in commercial real estate brokerage. In addition to its brokerage business (which includes property sales as well as appraisal & valuation), CBRE services leases and provides facilities management outsourcing, both of which are complementary to the brokerage business while also serving to reduce CBRE’s cyclicality. In all four of these businesses, CBRE is the market share leader. [7] Additionally, it generated 2016 revenues of $13.1 billion in global revenue versus its next biggest competitor, Jones Lang LaSalle, at $6.3 billion. Similarly, it has the most offices worldwide with 448 compared to only 286 at Jones Lang LaSalle.[8] This global network, which includes 201 offices in the Americas, 163 in Europe, the Middle East, and Africa, and 84 in Asia and the Pacific, reduces CBRE’s dependence on any one geographic region and also provides ample future growth opportunity as many of these markets are underdeveloped with only 12% of revenue coming from Asia-Pacific and 31% coming from EMEA despite 19% and 36%, respectively, of offices being located in these regions. Furthermore, the industry research firm Lipsey has named CBRE the number 1 commercial real estate brand in each of the last 16 years, and it’s been Euromoney’s Global Real Estate Advisor of the Year five years in a row. Finally, like insurance brokerage, another of our favorite brokerage categories, there are only a limited number of players with global scale in commercial real estate, which leads to a somewhat oligopolistic industry structure and thus more pricing power since a multinational corporation or institution has few global one-stop-shop choices. This structure creates a positive-feedback situation. As more and more multi-nationals choose CBRE, the company widens its lead over smaller global and regional players, leading to even more multi-nationals choosing them in the future.

The fourth and final reason we believe CBRE is a great business is that management’s interests and current strategy are aligned with long-term value creation. With over $25 million of stock as well as accountability to ValueAct (which owns 8.5% of the outstanding shares, possesses a board seat, and is one of the few long-term oriented activists), we believe CBRE’s CEO, Bob Sulentic, is properly incentivized. His strategic decisions since he became CEO in 2012 reinforce this view. Over the last decade, by intentionally increasing CBRE’s recurring revenue sources from 61% of total fee revenue in 2006 to 73% in Q2 2017, he and his predecessor have significantly decreased the cyclicality of CBRE’s revenue and profit streams.[9] The main driver of this recurring revenue share gain is CBRE’s increased investment, both organically and through acquisitions, in facilities management outsourcing. Besides providing a more stable revenue stream, CBRE’s focus on facilities management outsourcing business has increased its ability to manage all aspects of a customer’s real estate needs, boosting client retention and cross-selling opportunities. Additionally, recognizing the inherent network effects of brokerage and still-significant fragmentation of the commercial real estate brokerage industry, Sulentic is growing the size and scale of the core brokerage business through organic office growth as well as tuck-in acquisitions. Finally, despite the reduced cyclicality of its revenue streams, CBRE’s management team has kept its Debt/EBITDA and interest coverage metrics at lower, safer levels than CBRE maintained during the years leading up to the global credit crisis of 2008.

If CBRE’s future is so bright, why are investors fearful about the stock? As with many of the opportunities we’ve discussed in our past letters, we believe investors are overly focused on two short-to medium- term issues that they believe they can time their entry and exit around.

The first issue is related to the commercial real estate cycle. Like most other assets, persistently low interest rates have driven up commercial real estate prices, perhaps to unsustainable levels. Additionally, because of the length of the bull market and the loosening of credit standards by some market participants, many believe we are quite late in the credit cycle. While these arguments have merit, we believe there are counterarguments that are also reasonable. For instance, the global economic recovery since the credit and real estate crisis of 2008 has been very anemic relative to historical recoveries. Thus, we may not have built up the excesses necessary for a recession yet. Furthermore, people generally overestimate the risk of an event when a similar one has occurred recently and is particularly salient, and we believe the global financial crisis of 2008 checks both these boxes. Moreover, this overestimation may be further exacerbated by the fact that, unlike independent events such as the flipping of coins, financial crises generally result in the participants changing their behavior, at least for a time. In the case of the global financial crisis of 2008, these behavioral changes have included more regulation, less financial leverage, stricter underwriting standards, cost-cuts, an increase in non-cyclical business mix, and a less torrid pace of real estate development, all of which may have further reduced the odds of a real estate or credit crisis reoccurrence. As we detailed above, CBRE itself has taken many of these steps. In the end, as we have historically emphasized, we believe trying to predict the short-to medium- term prospects of the economy or markets is a fool’s errand, and we view significant market fear about the macro-economic environment as more likely to result in the underpricing of a great business than the overpricing of one.

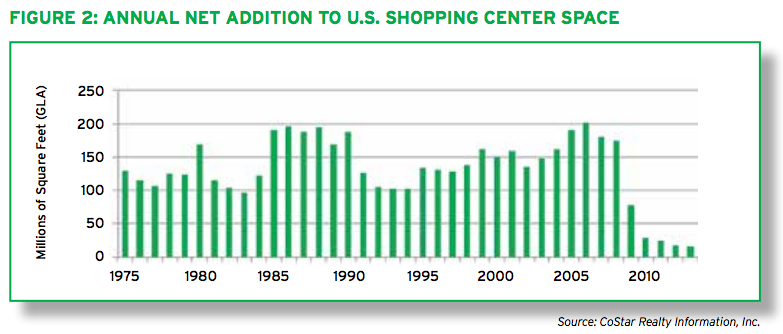

The second issue that concerns investors is the health of U.S. retail, which comprises 17% of total U.S. commercial real estate,[10] because of its high retail square footage per capita combined with explosive online sales growth.[11] While these are certainly potential issues, we would note a couple of less publicized facts that contradict this narrative. First, retail commercial real estate square footage growth has increased at a much slower pace than sales growth over the last 8 years.[12] In contrast to draconian predictions of massive retail store contraction, this data suggests that the more likely path to fixing capacity issues is a muddle-through scenario in which very slow retail square footage growth combines with steadily rising retail sales to gradually fill up any excess retail space.

Secondly, many subsectors of retail are performing quite well, with expected net store growth of 4,080 in 2017 and 5,500 in 2018 as well as revenue growth of $121.5 billion through the first seven months of 2017.[13] This growth leads us to question whether the U.S. even has a retail capacity issue. Indeed, while it’s possible that U.S. retail is massively overstored, we think it’s more likely that investors are making a classic error of overweighting high profile large losses and underweighting low profile but more numerous, and larger in aggregate, small gains. In other words, they are overweighting the sales woes and store closures of the high-profile failures (with just 16 chains accounting for 48.5% of the total number of stores closing and five of these 16 representing 28.1% of the total closings[14]) and underweighting the sales growth and store openings of the many smaller, newer retail concepts. The same sort of logic applies to globalization and the industrial revolution and their effects on wealth and jobs. While globalization has resulted in some high-profile job losses in certain sectors of the economy, most notably manufacturing, most economists and investors acknowledge the incredibly diffuse but, in aggregate, larger gains in wealth that the population has experienced in the form of cheaper goods and services. Most economists argue that this increased wealth has also resulted in more job opportunities since this new purchasing power increases the entrepreneur’s incentives to produce more existing or create new desirable goods or services. Similarly, despite destroying almost all farming jobs, the industrial revolution dramatically increased food production, countries’ populations, median and average wealth per capita, and job opportunities.

Moreover, don’t forget that online retailers need distribution centers and potentially brick-and-mortar stores as well. In fact, the winners in retail will probably be the ones that can master the all-channel solution, as Amazon itself has potentially foreshadowed through its Whole Foods acquisition. In our view, humanity’s increasing wealth will likely result, as it has historically, in more variety of services, goods, and experiences over time, not less, and we believe future job opportunities and retail shopping/store choices are no exception. In any case, even if we’re wrong about U.S. retail’s aggregate pricing and square footage growth, we believe that its size relative to total U.S. commercial real estate square footage combined with CBRE’s vast global growth opportunities make its cloudy future relatively unimportant to the long-term value of CBRE.

The logical next question to ask, when analyzing CBRE, is whether the concerns surrounding the health of the commercial real estate cycle and U.S. retail are properly discounted in the price. In contrast to the market participants who are trying to time their short-term entry and exit based on short-to medium- term macroeconomic and cyclical factors, we are focused on buying assets for less than what we believe they are worth and on holding them for a long time. Thus, our approach to these risks is to attempt to assess whether 1) the business is likely to be making significantly more money ten years from now under the vast majority of likely scenarios, 2) the return from owning the stock is likely to be good relative to our other stocks on a risk-adjusted basis, and 3) the combination of the company’s financial and operational leverage is conservative enough that we are very likely to make it through even a very bad economic environment with our ownership stake intact. Since we recognize that we can’t predict whether a cheap asset will become cheaper, if the stock meets these three criteria, we buy it. If the stock declines more and these three criteria continue to remain, we buy more.

In CBRE’s case, based on our view of its competitive advantages and growth opportunities, we ran various scenarios including a correction equal to 2008 occurring next year, in 5 years, and so on. Based on this scenario analysis, we believed the business was highly likely to be bigger and more profitable ten years hence. Additionally, based also on its very discounted valuation of less than 15x our estimate of recurring cash earnings (versus the mid-twenties multiple of earnings that many of our other portfolio companies commanded), we believed we were likely to get adequate long-term returns in almost all these scenarios. Thus, while CBRE has a broader probability distribution of future cash flows than our other holdings given its cyclical risks, we believed our forward expected rate of return was higher than in our average holding, compensating us for this additional risk and making CBRE’s risk-adjusted return comparable to our other investments. Finally, we think it’s very hard to construct a scenario where the company is forced to dilute our ownership given the change in the mix of recurring revenue combined with the lower leverage, making the probability of a catastrophic loss extremely low, in our view. Since CBRE passed all three tests (and, as an added bonus, diversified our portfolio cash flows), we bought it. If it turns out that we’re wrong about the probability of an imminent down-cycle in commercial real estate but that we still believe we’re correct in our assessment of the company’s competitive advantages, then we’ll buy more (unless, of course, an even more attractive opportunity presents itself).

Concluding Remarks

As our CBRE analysis demonstrates, our investment strategy relies on exploiting institutional and behavioral biases that cause market participants to shorten their investment time frames. Our ability to implement this strategy is in no small part due to you, our equally long-term-oriented clients. We thank you for partnering with us, and we will continue to work diligently on your behalf to generate the best long-term risk-adjusted returns we can.

As always, please feel free to call us with any questions or concerns. We are here to help.

Sincerely,

The YCG Team

Disclaimer: The specific securities identified and discussed should not be considered a recommendation to purchase or sell any particular security nor were they selected based on profitability. Rather, this commentary is presented solely for the purpose of illustrating YCG’s investment approach. These commentaries contain our views and opinions at the time such commentaries were written and are subject to change thereafter. The securities discussed do not necessarily reflect current recommendations nor do they represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. These commentaries may include “forward looking statements” which may or may not be accurate in the long-term. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable. S&P stands for Standard & Poors. All S&P data is provided “as is.” In no event, shall S&P, its affiliates or any S&P data provider have any liability of any kind in connection with the S&P data. MSCI stands for Morgan Stanley Capital International. All MSCI data is provided “as is.” In no event, shall MSCI, its affiliates or any MSCI data provider have any liability of any kind in connection with the MSCI data. Past performance is no guarantee of future results.

[1] For information on the performance of our separate account composite strategies, please visit www.ycginvestments.com/performance. For information about your specific account performance, please contact us at (512) 505-2347 or email [email protected].

[2] See https://dspace.mit.edu/bitstream/handle/1721.1/63255/100yearsofcommer00whea.pdf?sequence=1.

[3] Evidence that proximity generates more wealth includes economic studies on population density’s relationship to growth as well as the current distributions of real estate value and wealth between urban and rural areas. See https://www.ideals.illinois.edu/bitstream/handle/2142/26678/relationshipbetw538simo.pdf?sequence=1 and http://www.savills.com/_news/article/105347/198559-0/1/2016/world-real-estate-accounts-for-60–of-all-mainstream-assets.

[4] See https://www.eia.gov/consumption/commercial/reports/2012/buildstock/ and http://www.aei.org/publication/new-us-homes-today-are-1000-square-feet-larger-than-in-1973-and-living-space-per-person-has-nearly-doubled/.

[5] See http://www.prb.org/Publications/Lesson-Plans/HumanPopulation/Urbanization.aspx, http://www.un.org/en/development/desa/population/publications/pdf/urbanization/the_worlds_cities_in_2016_data_booklet.pdf, and https://www.fastcodesign.com/1669244/by-2050-70-of-the-worlds-population-will-be-urban-is-that-a-good-thing.

[6] See slide 11 in September 2017 CBRE presentation at http://ir.cbre.com/phoenix.zhtml%3Fc%3D176560%26p%3Dirol-presentations.

[7] See slide 1 in CBRE September 2017 investor presentation at http://ir.cbre.com/phoenix.zhtml%3Fc%3D176560%26p%3Dirol-presentations. Also, see https://www.cbre.com/about/media-center/rca-rankings-2016.

[8] As of December 31, 2016.

[9] See slide 5 in CBRE September 2017 investor presentation at http://ir.cbre.com/phoenix.zhtml%3Fc%3D176560%26p%3Dirol-presentations.

[10] See https://www.eia.gov/consumption/commercial/data/2012/bc/cfm/b1.php. For the purposes of the referenced calculation, we are defining total retail square footage as the total mercantile category plus food sales and services.

[11] See slide 6 at http://investor.ggp.com/sites/ggp.investorhq.businesswire.com/files/doc_library/file/Investor_Presentation_March_2017.pdf.

[12] See http://www2.census.gov/retail/releases/current/arts/ecommerce.xls, pages 3,4, and 5 in http://www.us.jll.com/united-states/en-us/Research/US-Retail-Outlook-Q4-2016-JLL.pdf, and http://kk.org/extrapolations/files/2016/08/ICSC-shopping-center-growth-1975-2014.png.

[13] See http://www.centromarca.pt/folder/conteudo/1700_7_Debunking-the-Retail-Apocalypse-Final-Enterprise.pdf and pages 7 and 8 in http://www.us.jll.com/united-states/en-us/Research/US-Retail-Outlook-Q4-2016-JLL.pdf.

[14] See https://www.chainstoreage.com/article/report-debunks-so-called-retail-apocalypse-more-stores-opening-closing/.

{kind=link}